The economy is facing one of its worst challenges. This development has put a lot of strain on businesses. The financial sector is also not sparred because the Domestic Debt Exchange Programme (DDEP) has impacted not only their profitability but also their capital.

This will make it difficult for Small and Medium Enterprises (SMEs) which are the backbone of the Ghanaian economy to survive particularly at a time when interest rates are above an average of 35 per cent. Non-performing loans as at last year has also increased to about 14 per cent. This means that, banks will tighten their risk structures before they lend to the SMEs

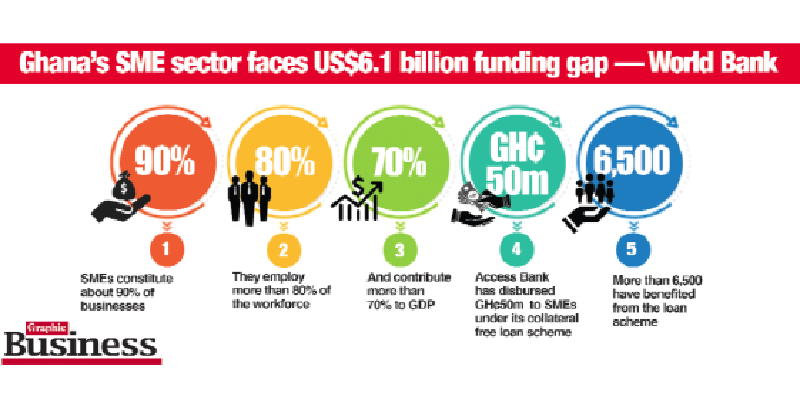

SMEs are a critical part of the economy. They represent about 85 per cent of businesses, largely within the private sector. Records indicate that, SMEs contribute about 70 per cent to the country’s Gross Domestic Product (GDP). These basic facts about SMEs in the country ,therefore, bears testimony to the fact that the sector has the capacity to completely or to a large extent, turn around the fortunes of the economy and the owners of small and medium businesses.

Considering the role of SMEs in national development and the financial challenges they are likely to face in these tough times, four ways by which SMEs can look attractive to the banks in order to easily access credit is discussed.

Business plan

Many people who want to start a small business fail to take the first step of having a business plan. It is simply a written document that describes in detail how a business—usually a startup—defines its objectives and how it is to go about achieving its goals. In short, it lays out a written roadmap for the firm from marketing, financial and operational standpoints.

There is a common allegation many such SMEs make. To them, banks refuse to lend funds to them to start or run their business. However, most of them fail to appreciate the fact that the money sitting with the banks are for depositors who have left their money for safekeeping and to earn some interest. Therefore, before a bank lends to an SME, it must be sure of who it is lending to and for what.

In effect, the bank must tell that the business is set up with an effective strategy for growth; it is able to determine its future financial needs and at least, it is able to attract investors which can be angel investors and venture capital funding or and lenders such as banks. Once a bank is convinced by seeing a serious business plan, it is confident to lend the money and even offer guidance.

This means that business plans are crucial for the success and survival of SME’s.

Bookkeeping

One of the basic mistakes many SMEs make is their inability to do one simple thing – bookkeeping. This means, there is no financials which the banks so badly require. But this is a very critical aspect of running a business. Simply put, bookkeeping is the process of keeping track of every financial transaction made by the business on a daily basis. Depending on the type of accounting system used by the business, each financial transaction is recorded based on supporting documentation. That documentation may be a receipt, an invoice, a purchase order or some similar type of financial record showing that a transaction took place.

In going for a facility, banks usually would want to see the books (financials) of the SME before they can have the confidence to advance funds to increase stock or for any other things which is business related.

Savings culture

To many SMEs, they can only save when the profits are big. Otherwise, deliberately setting aside bits of the day’s profit into savings is a no no.

There is a common saying that little drops of water makes a mighty ocean. Therefore, making it a habit to set aside a small percentage of profits made daily is crucial in that, over time, your saving culture will lead to building wealth and create opportunity for SMEs to access funds from banks.

Collateral

The term collateral refers to an asset that a lender accepts as security for a loan. Collateral may take the form of real estate or other kinds of assets, depending on the purpose of the loan. The collateral acts as a form of protection for the lender. That is, if the borrower defaults on their loan payments, the lender can seize the collateral and sell it to recoup some or all of its losses.

In Ghana like many other jurisdictions, this is required. As mentioned earlier, the monies with the banks is not for free. It belongs to people and business owners and, therefore, at the time they come for it, the bank must be able to pay. So at least, SMEs must ensure that they have something to prove as collateral so in case something goes wrong, there will be no burden on the bank.

Way forward

Some banks are doing a lot for SMEs to enable them to, at least overcome their financial hurdles.

For instance, some banks hold a lot of capacity building workshops and clinics for SMEs. These banks have special desks for advisory services.

Another intriguing thing has to do with the less rigorous loan access requirements. Some of these banks also ensure lending against turnovers with no tangible collateral but as the NPLs soar, a form of collateral is required and SMEs must watch that.

SMEs must, therefore, ensure that they adhere to the basic requirements as listed above. If in doubt, they can visit banks and financial institutions that are friendly and ready to advise on the way forward.

Source: graphiconline.com